The dry bulk market has been experiencing multi-year lows; the Baltic Dry Index (BDI) and its component sub-indices for the capesize, panamax bulk, supramax and handysize markets have been setting new lows by the day; the vessels are operating below operating break-even levels, and shipowners are going fast through their cash reserves or drawing down on their lines of credit.

Early in 2014, the dry bulk market was coming after a strong winter and with high hopes for the year; spring of 2014 brought a slowly declining market and by Posidonia 2014, the first signs of concern could be heard of at the beachside parties. The summer was tolerated as seasonally weak time of the year and all hopes were placed for a recovery in the autumn. The market then showed signs of recovery, very strong on occasion for the volatile capesize market, but really nothing to write home about on a sustainable basis. The turn of the year in 2015 brought more deliveries from the shipbuilders and strong growth for the world fleet, and any market recovery has been postponed further into the future.

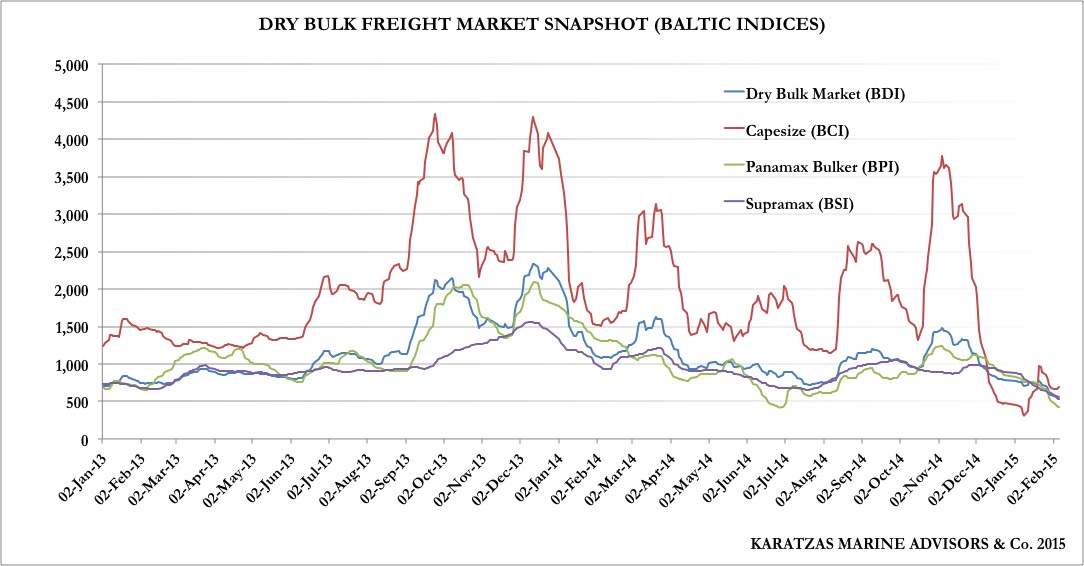

Dry Bulk Indices since 2013: False positive? Karatzas Marine Advisors & Co.

As per accompanying graph, the dry bulk indices have been setting new lows, with the BDI settling at 530 points on Friday Feb13rd (in early November 2014, the index was trading just below 1,500 points). The more volatile cape index had a more spectacular decline diving from almost 3,800 points in early November to 311 points in early January before bouncing a bit to 630 on Friday, February 13rd. Indices are only indicative of trends, rarely a scientific representation of the market (i.e. the Baltic indices represent freight rates achieved ignoring the number of vessels bidding for same cargo / idling vessels / vessels looking for cargo / fleet utilization, etc), and the current index levels only indicate a painful market generally.

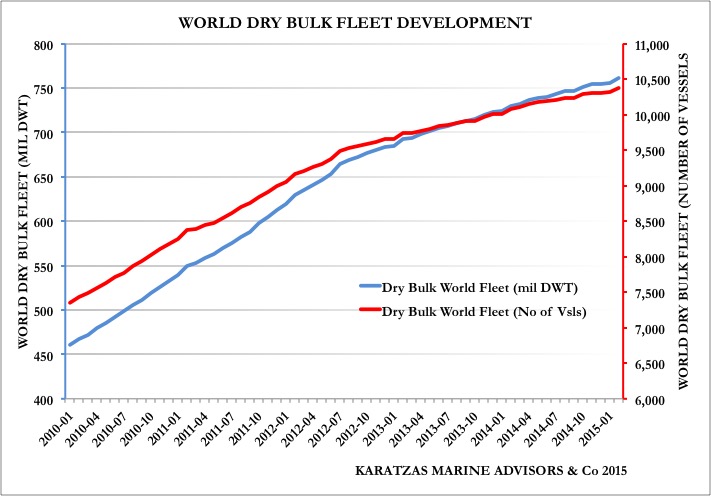

One can put the blame for the decline for the shipping industries to slowing growth in Japan, Europe and notably in China, increased political uncertainty with Europe and Russia, the strength of the US dollar, etc The main explanation however is that as early as 2010 when the market had started showing signs of life, there had been an ever increasing appetite for newbuildings, whether due to competitive newbuilding pricing, favorable payment structure, the promise of the eco-design, the desire to be the first mover in a market, urgency to lock up newbuilding slots before the competition, etc As per attached graph, from January 2010 to January 2015, the world’s dry bulk fleet grew by 300 million deadweight tons, from 460 to 760, a 65% total increase, or more than 12% annually. Likewise, the number of dry bulk vessels floating grew by 3,000 vessels to 10,300 vessels over the same time frame, for a total increase of 42%. Demand has not grown remotely by half of the supply growth, which may explain the state of the market.

World Dry Bulk Fleet Development (in deadweight and number of vessels) Karatzas Marine Advisors & Co.

Weakness in the freight market obviously will have repercussions throughout the industry, and it is already affecting many activities in the market, including the sale & purchase market. As one would expect, volume of transactions has declined, as potential buyers do not find it appealing acquiring vessels and right away having to contribute additional funds for operating the vessels. As the market has not found a bottom yet, buyers have gone on a “buyers’ strike” taking the time where asset prices will settle. For many owners it’s a scary market, but there are also well capitalized owners who have the money and they are always for the lookout for good deals, that is top quality tonnage at knocked-down prices. The last thing an owner wants is to overpay in a falling market, understandably. And, it’s a scary market for owners of vessels looking to sell. Chinese built vessels or vessels with less than perfect pedigree are automatically turned down, even at discounted prices; for sellers of good quality tonnage, they have to meet on price and terms the offers of the bottom-feeding buyers…Given that the market has been quiet for more than a month now, often, it’s hard to know where the market is (price discovery, as economists say) for many types of vessels.

An indicative round-up of sales in the last month or so:

In early January, it was reported that the capesize vessel MV „Nordtramp” (2001, 172,000 dwt, Koyo Dock K.K.) was sold to Seanergy in Greece at $17 mil; the vessel is relatively small compared to modern tonnage (ca 182,000 DWT), but she has a perfect pedigree of builder and previous ownership, but the price negotiated is a notable step down from previous transactions. She’s a 14-yr old vessel with approximately 10 years remaining economic life effectively and was sold a few millions above her scrap price; in the previous bottom of the capesize market in 2012, typically older vessels of 17-18 yr old vessels were selling at small premium to scrap; solely based on this transaction, it seems that the present bottom of the market is lower than the previous bottom, not a good sign for the market, if one believes in the art of charting the market. There are no additional sales of capesize tonnage this year, indicative of the dearth of activity in the market. There have been strong rumors that several capesize vessels have been marketed in the demolition market, and approximately a dozen of them have been committed to scrap buyers. Not that we are keeping score, but twenty capesize vessels have been delivered so far this year from shipbuilders, thus, even in a terrible market like at present, there has been a positive net growth effect on the world capesize fleet. There have been hopes that the present weak market will accelerate demolitions and decelerate newbuilding orders, but, having heard this lullaby before, it’s always wise to be skeptical. There also have been hopes that given the better prospects of the tanker market, many capesize (and other dry bulk) newbuilding orders will be converted to tanker orders; this may be a viable option, but it’s neither sure-proof nor inexpensive: just last week, publicly listed Scorpio Bulkers (ticker: SALT) converted three orders of capesize newbuildings to tankers and taking an immediate loss of $22 mil.

Panamax Bulker ‘Annoula’ under the Bosporus Bridge (same named vessel as the one reported transacted in this post; NOT the same vessel) Image source: Karatzas Photographie Maritime

The panamax dry bulk market has probably had the distinction of being the weakest of all dry bulk sectors; panamax bulkers barely earn a premium over the smaller supramax vessels, and accordingly, there is no price differentiation between panamax bulkers and supramax vessels of the same age; according to the Baltic Exchange Sale & Purchase Assessment Index (BSPA), a 5-year-old panamax bulker (74,000 DWT) sells at $19.33 mil, while a same aged supramax (56,000 DWT) sells at a slightly higher price of $19.62 mil. On indicative basis, the kamsarmax vessel MV „A MAX” (2011, 84,000 DWT, Hyundai Samho) was sold at auction at $16.55 mil to Greece-based Iolcos Hellenic Maritime Enterprises; the pricing is very weak, but cannot be considered representative of the market as this was an auction sale (typically auctions do not bring a premium), the vessel was at lay-up for more than a year, kamsarmax type vessels are not every buyer’s flavor, and also, this vessel has 235 m LOA (vs a typical 229 m LOA for kamsarmax tonnage). About a month ago, the kamsarmax vessel MV „BLUE MATTERHORN” (2011, 83,500 DWT, Hyundai Samho, 229 m LOA) was sold at $22.5 million. In late December, Scorpio Bulkers sold a prompt resale kamsarmax (N/B Resale Hull No SS-164, 2015, 81,000 DWT, Tsuneishi Zhoushan) at $30.7 mil, a sale believe to have taken place at a loss for the company. The panamax bulker MV „THALIA” (2001, 75,000 DWT, Hitachi Zosen) was sold by Greece-based Neda Maritime at $9.7 million to clients of Shelton Navigation. The panamax bulker MV „MARITIME TABONEO” (2004, 76,000 DWT, Imabari Shipbuilding) was sold at $10.8 mil by Shoei Kisen Kaisha to Cyprus Maritime. The older bulkers MV „ANNOULA” (1997, 70,500 DWT, Sanoyas) was sold at $6.1 million by Alpha Tankers & Freighters in Greece to Chinese buyers, and MV „THEOPHYLAKTOS” (1995, 72,000 DWT, Daewoo) by General Maritime Enterprises to Chinese buyers at $5.3 million.

The supramax dry bulk market has been exceptionally inactive with five transactions reported year-to-date; the transactions typically refer to vintage tonnage, vessels built in the previous century. MV „VERDI” (2007, 58,500 DWT, Tsuneishi Zhoushan) was sold in January at $15 mil, while the older MV „BIKAN” (2001, 52,000 DWT, Sanoyas) was sold at $9.7 mil.

The handysize market is usually more active as vessels cost less money and there is a longer tail of ownership worldwide; there have been approximately twenty transactions taking place so far this year, with most of the vessels being older or being built in the last century; noteworthy transactions have been the sale of MV „EGS TIDE” (2011, 36,000 DWT, Huyndai Mipo) at $16.85 million. The slightly older MV „CRESCENT HARBOUR” (2007, 32,000 DWT, Kanda S.B. Co) at $10.7 million. Same aged MV „DIAMOND OCEAN” (2007, 32,000 DWT, Hakodate Dock) was sold at $11.50 million by Daiichi Chuo.

All in all, the sale & purchase market for dry bulk vessels has been quiet, which is challenging for shipbrokers in markets specializing in the dry bulk markets; also, dropping asset prices and lack of market comparables make vessel valuations challenging; not to mention that shipping loans still holding covenants of vessel valuations and collateral are getting close to call.

The demolition market is not as active as the weak freight market would imply, but still much more liquid than other times in 2014. The demolition market has dropped since the beginning of the year, grossly dropping from $500/ldt to $400/ldt, or even slightly lower. This is a sizeable drop, precipitated by speculative transactions taking place in late last year for buyers of scrap vessels committing to vessels and prices and then having to re-negotiate lower when local conditions deteriorated, thus resulting in defaulted transactions pulling the market lower. The strength of the US Dollar (vessels are sold in US$ but local buyers have to price locally) and weak growth locally (reflecting lower steel plate pricing) have also contributed to the drop of the market as well. It’s to be seen how the demolition market will progress throughout the year; there is hope that demolition prices will be strong over the long term, but in the immediate term, it seems there is little steam in this market.

The dry bulk market will be an interesting market to watch in the coming years….

© 2013-2015 Basil M Karatzas & Karatzas Marine Advisors & Co. All Rights Reserved.

IMPORTANT DISCLAIMER: Access to this blog signifies the reader’s irrevocable acceptance of this disclaimer. No part of this blog can be reproduced by any means and under any circumstances, whatsoever, in whole or in part, without proper attribution or the consent of the copyright and trademark holders of this website.Whilst every effort has been made to ensure that information herewithin has been received from sources believed to be reliable and such information is believed to be accurate at the time of publishing, no warranties or assurances whatsoever are made in reference to accuracy or completeness of said information, and no liability whatsoever will be accepted for taking or failing to take any action upon any information contained in any part of this website. Thank you for the consideration.