In an effort to be more efficient and focused, from now we will report on this blog only pertinent transactions per market segment and asset class for s&p (sale & purchase market) that have occurred in the last couple of weeks. Transactions and transaction details in shipping are never as transparent and clear-cut as many an analyst or an appraiser may wish to think; having the benefit of time-lapse and fact-checking, we believe that reporting more accurately sales vs reporting them prompter is of greater service to our readership. Also, our reporting will be more structured by market segment and asset class going forward. Transactions will be purely reported herewith; commentary on market conditions and trends, discussion on transactions and developments and their significance will be posted at our sistership blog, Shipping Finance by Karatzas Marine. Please feel free to subscribe!

As always, shipbrokerage and shipping finance advisory is provide by our sponsor company, Karatzas Marine Advisors & Co.

Despite the summer seasonality in the sale & purchase market, the market overall has been active; in the dry bulk market, there is no humongous volume of vessel sales, but the freight market has been improving ever so slowly since late spring, and many buyers (or at least interested parties) are trying to call the bottom of the market. There is increased buying interest and activity in terms of inquiries and vessel inspections – which does not always translate to transactions; interest nevertheless remains respectable. There have been concerns that some ‘hot’ buyers are outbidding the competition by a few hundred thousand dollars, but overall the market remains very disciplined. There is strong focus on modern and high quality tonnage, and always within certain price discipline; older- or lower- quality tonnage keeps receiving high opportunistic and sporadic attention only.

In the capesize market, MV ‘Churchill Bulker’ (179,000 dwt, Hyundai Heavy, 2011) was reported sold by Denmark’s Lauritzen Bulkers to Greece’s Marmaras Navigation at region $34 million. A week or so earlier, sistership MV ‘Corona Bulker’ (179,000 dwt, Hyundai Heavy, 2011) was reported sold at same terms from same sellers to same buyers. Lauritzen Bulkers had mentioned in the last year that they would be looking to divesting of their dry bulk assets, and thus they are carrying through with these transactions; on the other hand, Marmaras Navigation had mostly been pre-occupied with their tanker fleet, but since earlier this year they have been buying into the dry bulk downcycle. They have a very good name for timing correctly the market in the past, thus it will be interesting to see whether the recent build-up of their dry bulk fleet would add onto their reputation. Similarly-aged capesize vessel MV ‘Houheng 2’ (179,000 dwt, HHIC-Phil at Subic SY/Philippines, 2011) has been sold at less than $31 mil from her Chinese owners (Henghou Industries (H.K.) Ltd.) to undisclosed European owners; the marked down on pricing is clear compared to the Lauritzen sales, as buyers are extremely preferential for quality tonnage; it’s further understood that despite her age, MV ‘Houheng 2’ had to undergo extensive engine repairs last year, confirming buyers pre-occupation with tonnage with unblemished pedigree. Also similarly aged capesize vessel MV ‘Blue Cho Oyu’ (180,000 dwt, Daehan, 2011) was sold by S. Korean interests to Mano Maritime Ltd. (Israel) at $33.5 million, a strong pricing given the vessel’s pedigree. Resale newbuilding MV ‘Glory Max’ (Hull No Shanghai Waigaoqiao 1335, 180,000 dwt at Shanghai Waigaoqiao with 2016 delivery) was sold by Gleamray Maritime to clients of Coberfelt in Belgium at $44 million. Older sistership capesize tonnage MV ‘Raiju’ and MV ‘Kohju’ (173,000 dwt, NKK SB, 2000/2001, respectively) were sold from the Mitui keiretsu to clients of SwissMarine and Winning Shipping, respectively, at appr. $9.7 million, each; prices achieved represent a precipitous drop from sale prices achieved just nine months ago, and it will be interesting to see how these two last transactions will play out for the buyers, given that pricing are just a premium to scrap but vessels have at least seven more years remaining economic life each.

In the panamax asset class, the post-panamax bulker MV ‘Umberto d’Amato’ (93,000 dwt, Jiangsu Newyangzi/China, 2011) was sold to German interests at just below $15 million. Sistership vessels MV ‘WelHero’ and MV ‘WelSuccess’ (93,500 dwt, Jiangsu, 2010) were sold en bloc by South Far Ocean Group Ltd. to European interests at $28 mil collectively.

Modern panamax bulker tonnage has seen increased buying interest with a series of transactions to report: MV ‘Asita Sun’ (82,000 dwt, Daewoo (DSME), 2012) at $20 mil to Greek buyers (Golden Union or Chandris) via bank sale; MV ‘Orion Pride’ (81,500 dwt, Hyundai Samho, 2011) at $19.7 million by Golden Bridge in S. Korea to undisclosed buyers (reported Golden Union in Greece); Golden Union has also been reported to be the buyer of a similar unit, MV ‘Bergen Trader’ (81,500 dwt, Sundong, 2011) by Nisshin Shpg.Co.Ltd. at appr. $19 mil; MV ‘Rainbow Ace’ (81,500 dwt, Guangzhou, 2012) at $16 million to Norwegian interests (Golden Ocean).

There have been sufficient sales of ‘traditionally’ size panamax dry bulk vessels as well: MV ‘Luyang Rising’ (76,500 dwt, Yangfan, 2012) was sold to German buyers at a relatively soft price of $15.5 mil (but with intermediate survey promptly due). MV ‘Rondeau’ (77,000 dwt, Namura, 2006) was sold to Omicron Ship Management in Greece at $13.8 million. MV ‘Kanishka’ (76,000 dwt, Tsuneishi, 2005) was sold at auction in S. Korea at a low price of $11.5 mil to Greek buyers (Sun Enterprises); the vessel has been at lay-up for some time now, and buyers will have to spend some money to bring the vessel back to a trading condition, which reflects the softness in pricing. By comparison, similar vessel MV ‘Grace Future’ (75,500 dwt, Universal, 2006) was sold to Greek buyers (A.M. Nomikos) at a very respectable $13.3 mil. Moving on to older tonnage, MV ‘Mahitis’ (75,000 dwt, Hyundai, 2001) was sold to Korean buyers (KLC) at a reported price of $8 mil., while 1998-built in Japan MV ‘Star Natalie’ (76,000 dwt, Sumitomo, 1998) achieved scrap-related pricing at ca. $4.2 mil.

A flower-y market? (Image credit: Karatzas Photographie Maritime)

On to the ultramax / supramax asset class, an interesting sale for M/V ‘Yangzhou Dayang DY216’ (63,500 dwt, Dayang/China, 2015) by Crown Ship Ltd. at ca. $22.5 mil to an institutional investor in the U.S. (Raven Capital); after many funds were burned, there have been no sales to institutional buyers in a long while, thus the transaction stands out; it also stands out for the institutional investors’ preference buying ‘cheap ships cheap’, which it has not been of great investment success strategy, at least so far. MV ‘KT Condor’ (58,5000 dwt, Tsuneishi Zhoushan, 2011) was sold by Kambara Kisen at ca. $14.5 mil to Greek buyers (Kondinave). Similarly aged MV ‘Daxia (57,000 dwt, 2011) was sold at auction in Malta at $11.5 mil (understand that the vessel has been at lay-up for several months now, thus, besides the auction discount, there is also the costs associated with bringing the vessel back to trading condition.) Marmaras Navigation has also been active in the supramax market with the acquisition of two sisterships MV ‘Hanjin Albany’ and MV ‘Hanjin Rostock’ (55,700 dwt, Hyundai-Vinashin/Vietnam, 2011) at a lowly $13 mil each. MV ‘Nord Reliable’ (58,500 dwt, Tsuneishi Cebu, 2008) by P&F Marine achieved $13.8 mil to clients of Sea Globe.

For older tonnage in the sector, MV ‘Medi Osaka’ (53,000 dwt, Oshima, 2003) was sold by Nisshin Shpg.Co.Ltd. at $7.8 mil., while the also Japanese-built supramax MV ‘Olympias’ (53,000 dwt, Onomichi, 2001) was sold at a bank-driven-transaction at $7.2 mil. by Petrofin to other Greek buyers. Similarly, MV ‘Speedwell’ (50,500 dwt, Kawasaki, 2003) was sold by Misuga Kaiun Co. Ltd to Greek buyers (DND) at ca. $7.8 mil.

The transactions reported above have taken place within the month of July, and it seems to be a rather decent volume of business. However, one has to take into consideration that July has been the best month the dry bulk freight market has seen in a while, thus there had been some pent-up interest; also, although there has been certain price improvement since out last report, there is little real news to send home. Besides, several of the transactions mentioned above were for vessels at lay-up, and/or at auction, and/or driven by banks, and several of the Japanese sales were for reasons beyond market considerations, thus not a great deal of ‘voluntary’ trading volume.

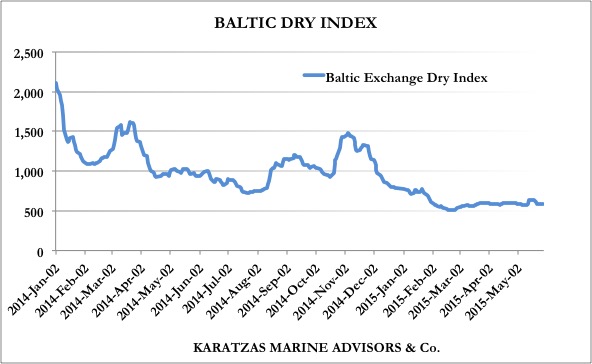

As a matter of hopeful thinking, the graph herebelow depicts the Baltic indices since the market bottomed in early spring. Just think positive, enjoy the hopeful chart, and do not let sinister thoughts disturb skin-dipping in your favorite waters in the summer!

Baltic Indices since February 2015.

© 2013 – present Basil M Karatzas & Karatzas Marine Advisors & Co. All Rights Reserved.

IMPORTANT DISCLAIMER: Access to this blog signifies the reader’s irrevocable acceptance of this disclaimer. No part of this blog can be reproduced by any means and under any circumstances, whatsoever, in whole or in part, without proper attribution or the consent of the copyright and trademark holders of this website.Whilst every effort has been made to ensure that information herewithin has been received from sources believed to be reliable and such information is believed to be accurate at the time of publishing, no warranties or assurances whatsoever are made in reference to accuracy or completeness of said information, and no liability whatsoever will be accepted for taking or failing to take any action upon any information contained in any part of this website. Thank you for the consideration.