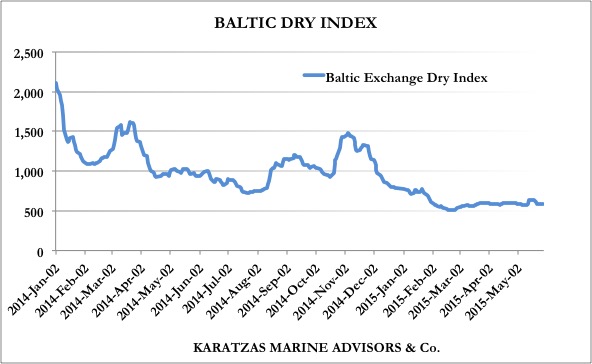

The shipping industry has been bobbing along ever since the financial crash of 2018. There is, of course, the expected market sector rotation with certain asset classes coming in and getting out of favor; at present, dry bulk vessels are cash flow positive, containerships rather weak, and tankers and offshore assets downright miserable. Following the whims of the freight market, values of ships fluctuate up and down; when certain sectors are out of favor, there have been sales on occasion at eye-popping low levels – and when the market improves, there may even be a chance for a shipowner’s favorite game, the famous “flipping of assets” to monetize on asset appreciation.

While the shipping market keeps doing what it does best – being volatile, shipping banks and capital for shipping are getting even tighter and costlier, which impacts not only vessel asset prices but also the volume of sale and purchase of vessels in the secondary market. For instance, at present, given the state of the tanker market, there have been months without the sale of tanker vessels in certain asset classes (there have been almost six months without the sale of modern VLCC, suezmax, aframax, LR2, MR2 and MR1 tankers that were not between affiliated parties or not subject to financing), which makes pricing and valuing of vessels all more complicated. All along, regulatory requirements keep piling on the industry (IMO2020 is the latest concern), while new technologies and innovation keep raising the technological risks for the industry.

Commercial considerations aside, the current state of the market is impacting not only vessel valuations but also the process of arriving at an accurate (and, some even say honest) vessel valuation. The standard definition of Fair Market Value (FMV) is premised upon the existence of a liquid secondary market; when the last comparable sale was six months ago, it might as well it had been six years ago given the volatility of the industry. As a result, delivering an accurate vessel appraisal when there is dearth of data, it can be considered an “art” at the very least, or worse, the subject of intense scrutiny of not only the outcome of the valuation but also of the process of the valuation, including questioning the qualification of the vessel valuator themselves. Valuation is not just the outcome, the value of something, but also, the qualification and the standards of the valuation process as well – the integrity of the process.

When times were easier for shipping… STS Leeuwin II in Fremantle, Perth, Australia. Image credit: Karatzas Images

Standard industry practice is that vessel valuations are commissioned from shipbrokers on the assumption that they have their finger on the pulse of the market. On the other hand, one has to keep in mind that there are concerns of the integrity of the process of deriving a number, especially when data is old and have to be “interpreted” and judgement comes into play. And, as uncomfortable as it is talking about it, there are conflicts as shipbrokers make much more money on commissions by selling vessels than providing valuations for vessels, thus, they may ensure when providing valuations to ingratiate themselves to the party that likely will give them more sale-and-purchase (“S&P”) business in the future. There are cases where shipbrokers and vessel valuators in the same shipbrokerage company are often at odds, given that they have conflicting interests: vessel valuations are a loss leader for many shipbrokerage companies (at a typical $1,000 per desktop valuation) while a commission of 1% on the sale of the same vessel can generate a much higher bonus. One does not want to upset the owner / seller of a vessel with a tight valuation of their property.

Of course, there have been online platforms whereby automated vessel valuations can be provided instantly via an algorithmic process. Such an automated approach would presume there is no bias, such as un-intentional personal judgement of interpreting the data or intentional skewing the results of the valuation to favor a certain party. While such a presumptions seem credible, on the other hand, one has to be aware that the algorithmic process is backward looking (historical data with historical bias), and still it has to depend on judgement as certain sales should be adjusted or disqualified since they may not be true comparable sales (judicial sales, auctions, subject to financing, sale-and-leaseback transactions, etc) In our experience, and convenience aside, algorithmic valuations overall do not provide much higher accuracy than qualified, unbiased actual vessel appraisers.

As we have discussed elsewhere in previous post, there are also additional valuation methods to be considered than the market comparable approach, such as the income approach method and the replacement cost method. However, such methodology often gets beyond the realm of expertise of a shipbroker as concepts of finance, economics, accounting, and possibly taxation may come into play. We have seen in the past, a partner at a shipbrokerage shop googling for Net Present Value (NPV) formulas in order to provide an income approach for a vessel valuation; we feel disheartened for such practices and for people being so cavalier with asset values; and, coincidentally, we would love to see such partner explain themselves in a court of law under oath in a scenario of litigation, where they would had to explain their methodology – when it’s clear they lacked any fundamental understanding for the valuation process. There is clearly legal liability for poorly prepared valuations.

Reflections on watery matters… Image credit: Karatzas Images

Most U.S. banks, leasing companies, commercial asset finance and equipment finance companies have now raised the bar for the firms and the people providing valuations; as such firms have a fiduciary duty to ensure that they look diligently after the money of their depositors and investors, it would make absolute sense that whoever is providing ship valuations has to meet certain academic standards, are subject to continuing education and that they have to abide by a set of professional rules and code of ethics. “Gray lenders” such as credit funds and other investment firms active in shipping seem to keep working with their preferred brokers, but this can be a liability claim in the waiting. The Securities and Exchange Commission (SEC) have been known to have taken an extra look in the last few years at certain publicly listed entities and their vessel valuation methodology and accounting practices. When investors lose money with their shipping investments, it’s hard to see what would stop them from pursuing legally asset managers for not credentialing properly their vessel valuation practices.

We do not want to be warmongers but in an environment of higher regulations for banks and investors, as well as people in shipping, one should be surprised to see how vessel appraisals are delegated as a matter of favor or a matter of inconvenience. Reality should be expected to soon catch up.

The sponsor of this blog, Karatzas Marine Advisors & Co., is pleased to announce that they have taken the matter of ship valuations or vessel valuations or ship valuations or ship appraisals – however valuation of marine assets is called, to a higher level. The firm employs Accredited Senior Appraisers (ASA) for Machinery and Technical Specialties who have met high academic standards, have passed qualifying exams, and most importantly, have to strictly abide to an extensive code of ethics. The firm also employs Fellows of the Institute of Chartered Shipbrokers (FICS) who have passed extensive exams and had to demonstrate years of experience in the maritime industry to qualify for such accreditation. Additional qualifications for the firm’s personnel include Accredited in Business Valuation (ABV) by the American Institute of Certified Public Accountants (AICPA) and Certified Marine Surveyor (CMS) by the National Association of Marine Surveyors (NAMS). The firm is a member of BIMCO and the Baltic Exchange among several professional memberships. The firm also employs Ivy League MBAs and graduates who can provide an income approach valuation without having to google the NPV formula!

© 2013 – present Basil M Karatzas & Karatzas Marine Advisors & Co. All Rights Reserved.

IMPORTANT DISCLAIMER: Access to this blog signifies the reader’s irrevocable acceptance of this disclaimer. No part of this blog can be reproduced by any means and under any circumstances, whatsoever, in whole or in part, without proper attribution or the consent of the copyright and trademark holders of this website.Whilst every effort has been made to ensure that information herewithin has been received from sources believed to be reliable and such information is believed to be accurate at the time of publishing, no warranties or assurances whatsoever are made in reference to accuracy or completeness of said information, and no liability whatsoever will be accepted for taking or failing to take any action upon any information contained in any part of this website. Thank you for the consideration.