The COVID-19 pandemic has been the low-probability-high-impact novel risk that few people had seen coming and warned about it (mostly statisticians and epidemiologists) but the greater business community had ignored it till now. Coping with COVID-19 is still an evolving process, and the shipping industry has been learning to react and adjust to the forces the pandemic has unleashed on supply chains and logistics, some with a positive impact, but mostly with adverse or very adverse implications.

We have argued elsewhere on some of those implications, and we will follow up soon with a few more thoughts. However, for now, the subject of marine asset pricing and vessel values, more than six months since the pandemic has started in the West, seems to be too intriguing to pass up.

Once the magnitude of the pandemic started taking shape by March 2020, and the extent of lockdowns and closing of borders and travel restrictions were evident, the first expectations were that this is going to be very bad for the shipping industry and for shipping values. After all, once the industrial base of China and the United States and the European Union coming to a screeching halt, and trade volumes collapsed, one had to expect the worst. And, indeed, the first couple of weeks of the pandemic were brutal in anticipation, from the world stock markets to the long lines snaking outside supermarkets.

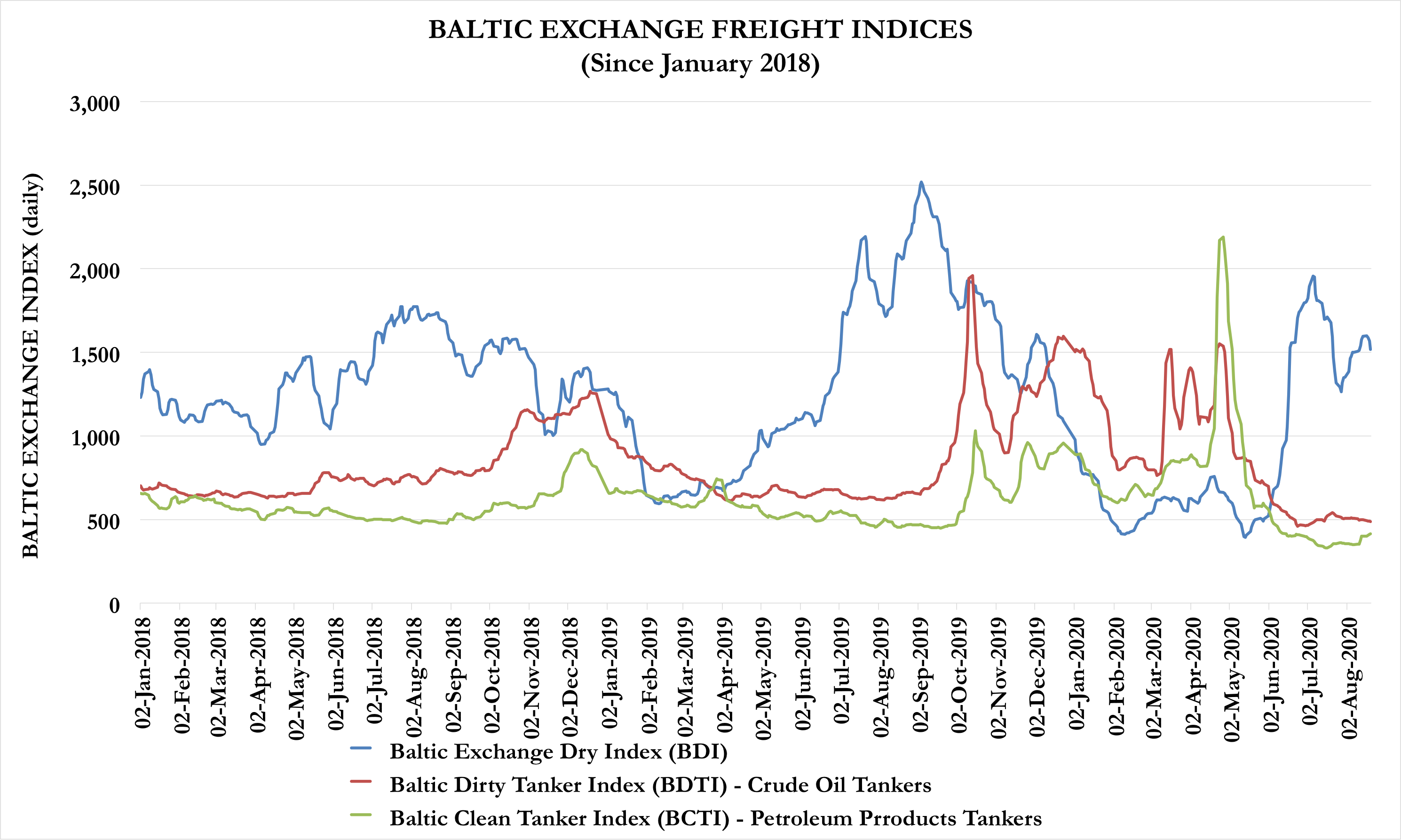

The Baltic Exchange [Disclaimer: Karatzas Marine Advisors is a Baltic Exchange member company] freight indices (both for dry bulk and tankers) were edging marginally higher at the beginning of the year on renewed hopes of market recovery. When COVID-19 smote the market, dry bulk freight rates quickly collapsed; it was not that demand for raw materials collapsed simultaneously with the rising of the pandemic, but port operations pushed forward any cargo requirements, thus pulling the freight market down fast in the short term. However, the very same disrupted port operations that pulled the freight market down had a completely different effect for tankers: combined with a glut of crude oil and petroleum products that brought the energy markets into a contango, and quickly tanker rates skyrocketed, at least temporarily. But, once oil companies and refineries managed to handle their excess inventory, as one would had predicted back in April, the tanker market deflated as well.

From the following graph of the Baltic Exchange Indices, freight rates presently are lower than at the same time last year (2019) and the year before (2018). There is a current, rather seasonal, rally in the dry bulk market (the US Dollar has lost appr. 10% of its value in 2020, and commodities priced in USD being cheaper in local currencies have spurred regional trades), but still below break-even cash levels. VLCCs are earning appr. $15,000 pd spot now (vs. $45,000 pd average 2019 earnings) and Capesize bulkers are earning $14,000 pd spot now (vs. $14,500 pd average 2019 earnings). Not great numbers, but again, as solace, in 2016 the market was much worse with Capesize vessels earning the grand sum of $4,500 pd. And, when considering the GDP of many OECD countries has dropped more than 10% in the first half of 2020, and the OECD formally expects global economic activity to drop by 6% to 7.6% annualized in 2020 (based on average scenarios), the current freight market is not bad at all.

Baltic Exchange Tanker & Dry Bulk Freight Indices since 2015

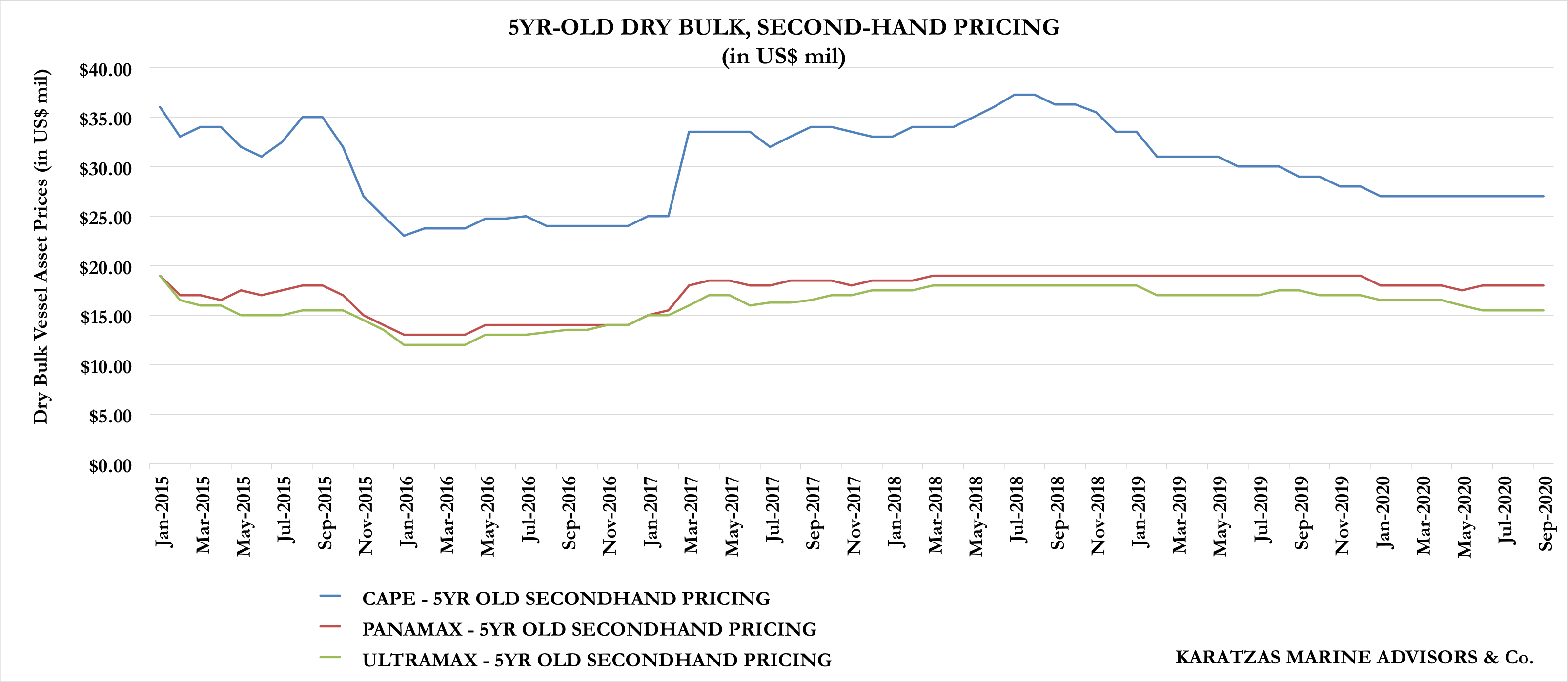

And, accordingly, since freight rates are highly correlated to marine asset prices, one’s attention turns to the secondary value of ships: at least the shipowners, and the shipping lenders and the investors as the use shipping asset prices as their main benchmark for equity (and wealth) creation, as collateral to shipping loans (Loan-to-Value or LTV) and the Net Asset Value (NAV) of the company. In the two graphs herebelow, we are using values of five-year old both dry bulk and tanker vessels, the major asset classes per market sector as a proxy, although prices for older and newer vessels show similar characteristics. The data were provided by the Baltic Exchange and Karatzas Marine Advisors.

For Capesize, Panamax and Ultramax dry bulk vessels, asset prices have declined since last year; in a sense, this is to be expected given the state of the market, but nominally, one would expect that dry bulk vessel prices to be lower at present than where they really stand. Not only freight rates are low, but also several complimentary factors (i.e. momentum, financing, etc) are worse than the freight market may imply. What is noteworthy is that although the overall marine asset pricing curve is negative, in the last several months, it’s effectively flatlined, showing signs of minimal variance and volatility. If the shipping industry is known for one thing is that it’s that flat lines rarely exist in shipping.

Tanker Vessel Assets Prices (5yr-old Vessels)

Likewise for tanker asset pricing, for five-year old VLCC, Suezmax, Aframax, Panamax LR1 and Medium Range MR2 and MR1 tankers, the overall trend is negative, but again, the several last months show a flat line as well. Minimal movement in tanker asset pricing, in a market that is known to move around widely.

Dry Bulk Vessel Assets Prices (5yr-old Vessels)

If any conclusions could be drawn from the current pricing activity (and a weak secondary market activity in the sale & purchase market) is that there is a tug of war between buyers and sellers that currently stands at equilibrium. Both buyers and sellers trade along the status quo and “last done” pricing as neither group has the upper hand. Despite the weak freight market, sellers still earn enough to pay their bills (and possibly their lenders, too), and buyers do not really have a reason to pay up to acquire tonnage (but also, they do not find “distressed” opportunities to feast on).

We would think that the market is bound to move, and rather strongly, in either direction in the near future. Both industry idiosyncratic variables (financing, banks, newbuilding activity, etc) or exogenous variables (the upcoming elections in the US are expected to be unusually contentious and impactful worldwide) could move the market and marine asset values, and the current boredom in the vessel value pricing is deceiving.

———————————————————————————————————

EFFECTIVE IMMEDIATELY, NEW BLOG POSTINGS ON SALE & PURCHASE MATTERS WILL APPEAR ON KARATZAS AUCTIONS –

PLEASE FEEL TO FOLLOW US THERE!

———————————————————————————————————

© 2013 – present Basil M Karatzas & Karatzas Marine Advisors & Co. All Rights Reserved.

IMPORTANT DISCLAIMER: Access to this blog signifies the reader’s irrevocable acceptance of this disclaimer. No part of this blog can be reproduced by any means and under any circumstances, whatsoever, in whole or in part, without proper attribution or the consent of the copyright and trademark holders of this website.Whilst every effort has been made to ensure that information herewithin has been received from sources believed to be reliable and such information is believed to be accurate at the time of publishing, no warranties or assurances whatsoever are made in reference to accuracy or completeness of said information, and no liability whatsoever will be accepted for taking or failing to take any action upon any information contained in any part of this website. Thank you for the consideration.