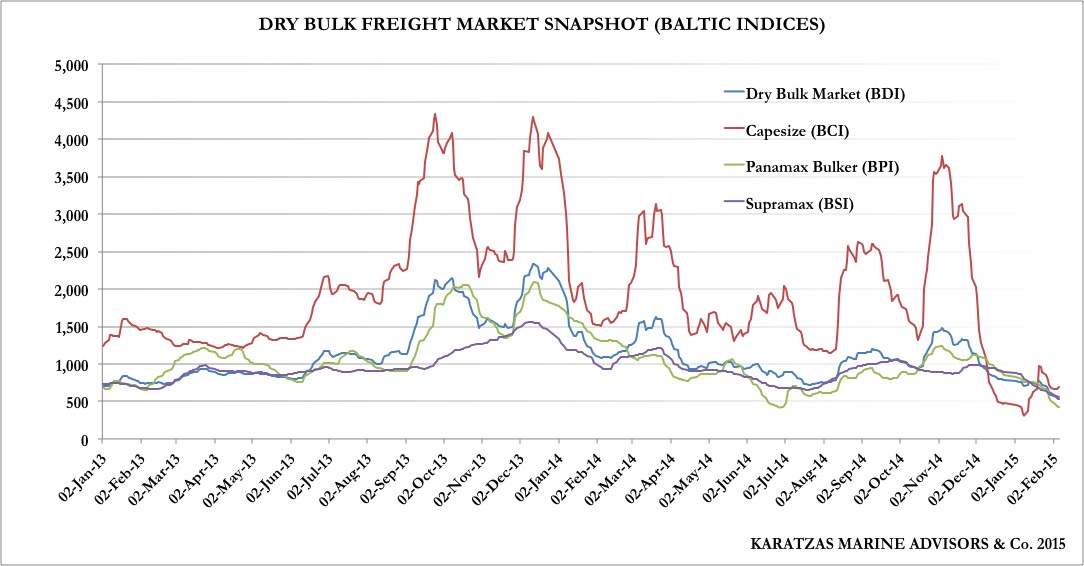

The last couple of weeks have brought the slimmest hope that springtime may be forthcoming for the much beleaguered dry bulk market; we are not talking about signs of an impending great recovery, but at least the dry bulk indices have stopped dropping and have shown marginal improvement; the widely-observed Baltic Dry Index (BDI) established an all-time low point on February 18th at 509 and closed at 591 on Friday March 20th; on percentage terms the improvement seems impressive (close to 20%), but again one has to keep in mind that the low of 509 was a thirty-year low – almost, and despite the improvement, dry bulk vessels are earnings below cash break even rates – thus, the improvement is not financially meaningful; it only bears psychological significance that hopefully the worst is behind us, for now.

As one would expect, publicly listed dry bulk companies continue to report abysmal earnings (actually losses), and earnings conference calls tend to range from confessionary litanies to Christmas lists on what would turn the market around. There have been the occasional corporate bankruptcy here and there and some ship arrests on a limited basis but nothing of a Korea Line Company (KLC) magnitude shockwave. Likely another blowup the size and significance of KLC will not materialize in the dry bulk market as KLC had taken shiploads on vessels at sky-high rates prior to 2008 while most of the traders / charter-in operators today have established their cost floors and rates at substantially lower rates in 2012 to 2014.

Supramax Bulker ‘Star Epsilon’ passing the Statue of Liberty in the New York Harbor; image source: Karatzas Photographie Maritime

While the dry bulk handysize, supramax and to a lesser extent panamaxes were slowly improving for a couple of weeks now, capesize vessels are kept on a freight declining route; only this week capes bounced from a low of 357 points to 423 points in a matter of two days, generating suspense for the coming week whether the freight rates will keep moving higher. It may be so, and it will be most welcome news; however, over the longer term, capesize tonnage likely will have a tough ride: the Chinese economy has both been slowing down and also getting shifted from industrial production to consumption which does not bode well for iron ore imports and the cape market; further, China has been producing (and storing) much more steel that can use and recently there have been talks of China dumping below cost steel to the international markets raising the prospects that the World Trade Organization (WTO) may be asked to look into the complaints; the fact that mining companies have been building up their own captive fleets and that Vale managed to find a resolution with China and Cosco for their so-called Valemax fleet is not boding well for the overall capesize market and the independent owners. A boost to the capesize market is much needed and hoped for, but on the long term, one has to be skeptical of too rosy prospects.

In terms of sale & purchase activity in the dry bulk markets, at present, actual activity is low; there is lots of ‘browsing’ and ‘interest‘ for buying quality vessels but little of such interest is translated to actual transactions; buyers are trying to find a ‘balance’ of not buying too early when bulkers can further drop in pricing, but, on the other hand, they do not want to miss out when the market recovers; it seems a patience search of the absolute bottom in asset prices is the name of the game. Few transactions can be reported in the dry bulk market and mostly for small, older, cheaper vessels (in absolute terms); given the lack of benchmark transactions is hard to place an accurate estimate of asset price decline; however, the trend is apparent that based on the transactions reported the market keeps heading lower.

In the capesize market, the sale of MV „Cape Stork” (171,000 dwt, IHI, 1996) was reportedly at close to $7.8 mil, a scrap related price level; interestingly, the vessel was sold in November 2014, less than six months ago, at excess of $15 mil, implying that the buyers’ bet then on a seasonal recovery for capes during the holiday season has not played out as expected. In another interesting transaction in the sector, Oaktree has sold at $80 million apiece two VLOCs MV „Selma B“ and MV „Camilla T” (320,000 dwt, HHI, 2010/ 2011, respectively) to Olympic Shipping (Onassis Group) to be converted to VLCCs; Oaktree was involved with the vessels during the restructuring of Nobu Su’s TMT (Today Makes Tomorrow); during the last year, the Onassis Group has shown to be an active buyer of tonnage, primarily in their historically beloved tanker market; however, the pricing for these vessels seems to be too strong given the costs, risks and ‘hair’ involved for the conversion project, not mentioning the concern that typically converted vessels do not seem to get special attention for the remaining of their trading lives by the charter market.

In the panamax bulker market, the post-panamax bulker vessel specialized for the coal trade MV „Sekiyo” (91,500 dwt, Hitachi, 1998) was sold at close to $9 million to Chinese buyers by Nippon Yusen Kaisha (N.Y.K. Line); the price is at premium of a couple million to scrap pricing, which is the norm these days for tonnage built prior to 2000. In the same sector, MV „Lopi Z” (72,000 dwt, Shin Kurushima, 1998) was sold to Norwegian investors in a sale-and-lease back transaction from Dalomar Shipping in Greece at approximately $6 mil, a purely scrap related price.

Supramax Bulker ‘Bulk Colombia’ in the Port of Hamburg; image source: Karatzas Photographie Maritime

The supramax market has proven the most active in the dry bulk market, with the sale of MV „C.S. Rainbow” (55,700 dwt, Mitsui, 2006, 4x30T cranes) at $11.25 mil by Japanese sellers to Greeks buyers (Blue Seas). The sale seems to be well below the price achieved by same sellers of similar vessel MV „Sunny Ace” (55,800 dwt, Kawasaki, 2005, 4x30T cranes) at $11.3 mil one month ago (vessel was also SSDD due.) Looking further back in January, when MV „VERDI” (2007, 58,500 DWT, Tsuneishi Zhoushan) was sold at $15 mil, the trend in supramax bulker pricing is clear. It’s really very hard to comprehend that ten-year-old supramaxes were selling at more than $60 mil in the spring of 2008 and at $22 mil just one short year ago; now we are talking about $10 – $11 mil for a ten-year-old vessel. The ten-year-old handymax MV „Ramada Queen” (46,000 dwt, Oshima, 2005) with drydock due sold at an eye-popping price of $8.7 mil to Greek buyers (Primal). The older handymax MV „Valopoula” (45,500 dwt, Tsuneishi Cebu, 2000, 4x30T) was sold at a respectable but still scrap related pricing of $6.1 mil to Greek buyers again (Dianik Shipping) with drydosck due. The smaller and meaningfully older handymax MV „Bay Ranger” (43,500 dwt, Oshima, 1995, 5x25T cranes) was sold at appr. $4.5 mil with the vessel recently having been drydocked (present estimated scrap value of about $3.1 mil at 7,350 ldt.) The similar vessel MV „Hellenic Horizon” (44,800 dwt, Halla, 1995), 4x25T cranes) was sold at a scrap related $3.7 mil – with drydock promptly due.

As one can note, recent transactions in the dry bulk sale & purchase market resemble rather a scrap report, with vessels sold between 10-20 years old and no modern tonnage to report on, drydock position and estimated scrap price always as points of reference. And the prices achieved resemble prices for vessels selling for scrap rather than further trading, another indication that buyers opt to act only when there is little downside risk with their acquisitions, either with vessels with 5+ years of trading life at scrap pricings on a minimal pricing over scrap and drydocking for vessels having a decent survey position.

Can things get more difficult?

© 2013-2015 Basil M Karatzas & Karatzas Marine Advisors & Co. All Rights Reserved.

IMPORTANT DISCLAIMER: Access to this blog signifies the reader’s irrevocable acceptance of this disclaimer. No part of this blog can be reproduced by any means and under any circumstances, whatsoever, in whole or in part, without proper attribution or the consent of the copyright and trademark holders of this website.Whilst every effort has been made to ensure that information herewithin has been received from sources believed to be reliable and such information is believed to be accurate at the time of publishing, no warranties or assurances whatsoever are made in reference to accuracy or completeness of said information, and no liability whatsoever will be accepted for taking or failing to take any action upon any information contained in any part of this website. Thank you for the consideration.