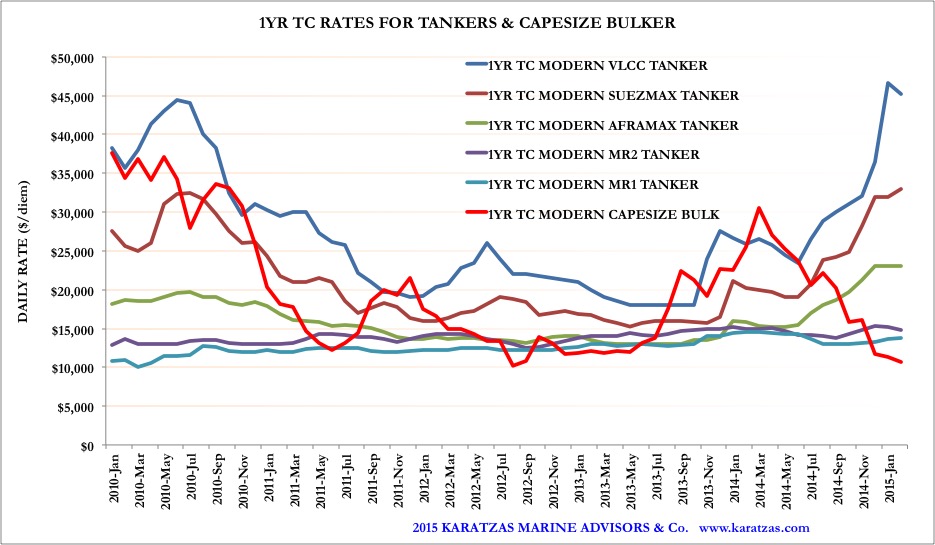

Unlike the dry bulk market which is experiencing a multi-cycle structural weakness, the tanker market has been behaving much more enthusiastically, at least for time being. Tanker vessels have been trading above operating earnings since early 2014, and on occasion, for spot rates, earnings have been eye-popping – such as when in January 2015 rates for VLCCs flirted with the $100,000 pd mark. The attached graph shows one-year time-charter rates for the major segments in the tanker market, including the capesize market, for purposes of illustration and comparing tanker and dry bulker markets; and an obvious reminder, capesize vessels are the largest commoditized bulker vessels in the business.

Crude oil pricing has grossly halved in the last year, and OPEC’s (read, Saudi Arabia’s) decision in November in Vienna to go after market share rather than margins has ensured that at least in the short term, oil will be cheap and likely will be trading heavily. Cheaper crude oil pricing has the potential of contango (buy now in the physical market, store – ideally on tankers – and sell in the futures market at a higher price); cheap oil pricing has the prospect of increasing demand (there are already signs that sales of SUVs and trucks are on the up in the USA) that eventually will mean more movement of cargoes; cheap crude oil has been encouraging build up of strategic petroleum reserves, and there are indications that China is going strong at building up theirs under the weakness of the pricing of the commodity. A brutal winter in the USA has stimulated the use of gasoline which has affected positively the petroleum products trade in the Atlantic. Despite the shutting down of many drills in the US for shale oil production (down by 39% from 1609 to 986 operating drilling rigs between October and end of February, according to Baker Hughes), the US maintains sky high inventories of WTI crude oil (for the week ended on February 27th, US crude oil inventories showed a massive weekly build-up of 10.3 million barrels to a total of 444.4 million barrels); if not for the shale oil production, the seasonal impact of the inhumane winter would have a much pronounced impact on the crude oil tanker market.

The strength of the tanker freight market has stimulated increased dealing in the sale & purchase market, but mostly it has encouraged several ‘corporate’ transactions whether on the M&A front (Euronav acquiring the Maersk VLCC fleet, the ‘merger’ of the Navig8 VLCC fleet with General Maritime to create Gener8, DHT’s acquisition of Samco Shipholding’s VLCC fleet) and on the IPO front (earlier this year Euronav was successful finally obtaining a public listing in the US). While more M&A in the tanker market may be expected, IPOs can be a trickier market, as investor appetite can gyrate faster than the fortunes for freight for big tankers. There is increased interest to see how a few of PE-sponsored tanker shipping companies will proceed in this environment, which while promising, it does not allow for these companies to float at a profit – indicatively, both Diamond S. sponsored by Wilbur Ross and Principal Maritime sponsored by Apollo – have relatively high cost basis and a floating at NAV will result in realizing losses, at least in the short term. Investor interest, and also charterer interest, in the tanker market – despite the market’s strength – have been of concern to many a shipowner. For instance, while the spot market is very respectable, there is no period market – in general – as charterers prefer to pay up spot prices now but not willing to commit for a two-year charter. This observation does not bode well for the future of the market, when charterers do not have the conviction to commit for two years of rates – in hot markets or markets expected to break out, charterers want to act and cap their exposure.

Likewise, the activity in the secondary market has not been as active as the freight market would suggest; of course, banks do not lend easily these days, thus this is a dislocation affecting overall activity in the market. And the freight market is not as strong to support modern tonnage for operating expenses (OpEx) and a fully amortizing loans; by revisiting out graph at the top of the page, one-year TC for a modern VLCC is appr. $45,000 pd; given a nominal price of a VLCC tanker of approx. $100 mil. and approx. $9,000 pd OpEx, the earnings barely cover a fully amortizing ship mortgage. And, sale and purchase activity has overall been anemic – despite the strength of the market; and it’s clear that the focus of the transactions has been concentrated on modern vessels [typically vessels newer than five years old – suitable for publicly traded companies that are ‘hot’ for deals in this market and pay with equity (thus low leverage / more flexibility with cash flows), and vessels older than twelve years old at often prices at a multiple of scrap – by Asian buyers or buyers with access to cargoes]; these typically are not signs of a very liquid, solid market that has consolidated and about to break out; not to mention, that now that the freight market has improved, there have been packages of very modern tanker tonnage discreetly mentioned for sale, primarily from ‘OK’ owners or ‘OK’ / Chinese yards who are testing the market to offload positions at a small loss or at a break-even; once again, an indication of little faith in the prospects of the market, albeit from ‘weak hands’ or ‘OK’ quality tonnage with little prospects to be much sought after in the future.

On indicative purposes, since the beginning of the year, the following representative transactions have taken place: in the VLCC market, MT „Patris” (298,500 DWT, Daewoo, 2000) was sold by Chandris (Hellas) in the UK to clients for Modec for FPSO conversion at the relatively very strong price of $38 million; similar vessel, MT „GC Haiku” (299,000 DWT, Hitachi Zosen, 2000) was sold at $31 million by GC Tankers to New Shipping; the three-year newer MT „DS Voyager” (309,000 DWT, Samsung HI, 2003) was sold by DS Tankers to NG Moundreas in Greece at $42 million.

In the Suezmax tanker market, in 2015 so far, there has been only the sale of two sistership vessels MT „Chapter Genta” (156,000 DWT, Jiangsu Rongsheng, 2010) and MT „Roxen Star” (156,000 DWT, Jiangsu Rongsheng, 2009) at $96 mil from Roxen Shipping to interests controlled by Frontline / Fredriksen Group.

Likewise in the aframax tankers, Teekay Offshore has disposed of the shuttle tanker MT „Navion Svenita” (106,500 DWT, Koyo Dock, 1997) at an undisclosed price; MT „Sark” (113,000 DWT, New Times SB, 2009) has been sold by Sark Shipping to EA Technique at $40 million.

LR1 Products Tanker MT ‘Compass’ and cruiseship MV ‘Queen Mary 2’ in the New York Harbor in August 2014. Image source: Karatzas Photographie Maritime

In the LR1 tanker market, Prime Marine of Greece has sold four LR1 tankers to Hafnia Tankers in Denmark at an undisclosed consideration; the vessels were MT „Arctic Char” (75,000 DWT, Brodosplit, 2010) and the sisterships MT „Karei”, MT „Kihada” and MT „Maguro” (74,250 DWT, STX SC (Jinhue) 2010).

The MR2 product tanker market has been more active with the sale of sistership tankers MT „Caletta” and MT „Calafuria” (51,500 DWT, Hyundai Mipo, 2011 / 2010, respectively) by G. D’Alesio in Italy to interests at $30 mil each. For pumproom design vessels, Minerva Marine of Greece acquired MT „Nord Obtainer” (47,500 DWT, Onomichi Dockyard, 2008) at $19.50 mil, while similar tonnage vessel was sold to clients of Benetech in Greece at the comparatively high price of $23 mil for MT „Nord Star” (45,900 DWT, Shin Kurushima, 2009) from Saito Kisen. MT „Hellas Symphony” (46,200 DWT, Hyundai Heavy, 2000) was sold by clients of Latsco in the UK at $10.5 million, while similar tonnage MT „Tosca” (47,500 DWT, Brod. Trogir, 2004) was sold at $18 million. The 1997-built tanker MT „Midnight Sun” (45,000 DWT, Minami Nippon, 1997) was sold from Mitsui OSK Lines in Japan at $8.0 million to Far Eastern interests.

There has been an interesting sale of an MR1 tanker, MT „HC Elida” (37,500 DWT, Hyundai, 2001) at $11.5 million by Marlink Shif. in Germany to Far Eastern interests, showing relative strength for this under-the-radar tanker segment.

There have also been a few transactions in the usually quiet market for stainless steel tankers, such as the sale of MT „HF Pioneer” (19,900 DWT, Fukuoka SB, 2010) by Fairfield Chemical in the US to clients of Heung-A at $25.25 million. The also stainless steel tanker MT „Fairchem Colt” (19,900 DWT, Usuki Zosensho, 2005) by Tanba Kisen to S. Korean interests at $19 million. The older stainless steel tanker MT „ST Dawn” (19,900 DWT, Shin Kurushima, 2000) was sold by Stalwart Tankers at $14.5 mil to clients of TPL Shipping. The IMO II/III epoxy-coated tanker MT „Sichem Onomichi” (13,000 DWT, Sekwang, 2008) was sold at $11 million by Hisafuku Kisen K.K to S. Korean interests.

Once again, despite the fairly encouraging freight market, rather few transactions have taken place in the secondary market for tankers, and mostly for tonnage either newer than five years or older than twelve years.

And keeping accounts for newbuildings, eleven VLCC tankers have been ordered in 2015, twelve orders for Suezmax tankers and fifteen orders for Aframax tankers, and four MR tankers have been placed. All in all, TWO WHOLE VLCCs were scrapped so far this year, and zero scrappings in the rest of the tanker segments mentioned in this report, for a NET GROWTH of the world tanker fleet. It seems that staying away from NBs and more orders for tonnage is hard to do… And, a quick remark on the demolition market that has dropped by 20-25% since the beginning of the year, given the weakness of the dry bulk market and plenty of vessels offered, thus driving supply up and prices lower, admittedly from speculative rates well in excess of $500/ldt at the beginning of this year.

© 2013-2015 Basil M Karatzas & Karatzas Marine Advisors & Co. All Rights Reserved.

IMPORTANT DISCLAIMER: Access to this blog signifies the reader’s irrevocable acceptance of this disclaimer. No part of this blog can be reproduced by any means and under any circumstances, whatsoever, in whole or in part, without proper attribution or the consent of the copyright and trademark holders of this website.Whilst every effort has been made to ensure that information herewithin has been received from sources believed to be reliable and such information is believed to be accurate at the time of publishing, no warranties or assurances whatsoever are made in reference to accuracy or completeness of said information, and no liability whatsoever will be accepted for taking or failing to take any action upon any information contained in any part of this website. Thank you for the consideration.

Dear Basil, Thank you very much this excellent article. Kindest regards, Gianfranco From: Karatzas Shipbrokers RegisterSent: Monday, 9 March 2015 1:55 AMTo: gianfrancomeza@gmail.comReply To: Karatzas Shipbrokers RegisterSubject: [New post] S&P, Newbuilding and Demolition Update (March 8th, 2015) â Tanker Market Focus

a:hover { color: red; } a { text-decoration: none; color: #0088cc; } a.primaryactionlink:link, a.primaryactionlink:visited { background-color: #2585B2; color: #fff; } a.primaryactionlink:hover, a.primaryactionlink:active { background-color: #11729E !important; color: #fff !important; }

/* @media only screen and (max-device-width: 480px) { .post { min-width: 700px !important; } } */ WordPress.com

Karatzas Marine Advisors & Co. posted: “Unlike the dry bulk market which is experiencing a multi-cycle structural weakness, the tanker market has been behaving much more enthusiastically, at least for time being. Tanker vessels have been trading above operating earnings since early 2014, and on”