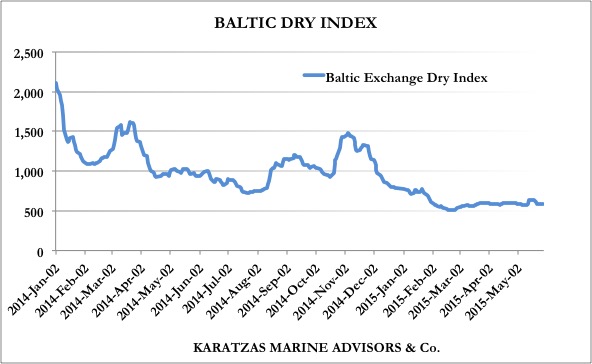

Since our last report at the end of September, the overall dry bulk market has dropped by more than 25%; however, when the decline is seen from the interim peak in early of November at 1,484 points to the present reading of 788 points, for the BDI, the index been cut in half (Graph 1).

Graph 1: Baltic Dry Indices since September 1st, 2014; (data source: The Baltic Exchange)

The capesize market as always has been the most volatile component of the BDI index, and it has been on a free fall from the top of 3,781 points on Nov 4th to 474 points on Christmas’ Eve, equating to less than $5,000 pd in terms of freight rates. Looking back, it was in late fall 2013 when the capesize index was trading at comparably high levels (as high as 4,500 points on an occasion), but 2014 has not been a good year for the dry bulk market overall. The performance of the dry bulk market in 2014 got many market players by surprise, as the consensus thinking had been that the market had found bottom in 2011 and 2012, and since then the trend was expected to be upwardly leading, only the degree of the positively sloping line was a matter of debate. The performance of the dry bulk market has been having a major impact on market activity, both directly and indirectly. For starters, cash flows have been at or below operating levels, thus dry bulk owners have been bleeding cash from running their dry bulk vessels, which obviously is not a good result. Further, given that dry bulk vessel ownership is much wider-ly spread (than let’s say tanker vessel ownership), the pain of negative cash flows is widely felt, affecting many, many owners in absolute terms, financially; and when the cash register of a great deal of owners bleeds cash collectively, momentum and attitude are negatively impacted, thus turning the mood of the overall market sour. Again, the consensus thinking has been that 2014 ought to be a good year and many players had placed accordingly ‘long bets’, thus the negative performance has an amplifying effect on a wide range of prospects from newbuilding orders placed on the assumption of an asset play game (surprisingly, no financing in place for many of these speculative orders) to companies having prepared for IPOs and access to the capital markets, to private equity (PE) funds expecting on building a positive track record with an eye to a quick and profitable exit strategy.

Graph 2: Baltic Dry Indices since January 2013; (data source: The Baltic Exchange)

The dry bulk index started the year in an active way with the tailwinds of last year, and until the middle of spring 2014 (Graph 2), the prospects were looking up; by partying time at Posidonia in June in Greece, the dry bulk market was more than a couple of months in decline; however, owners having built cash reserves during a strong 2013, were holding high hopes and were thinking of bridging the seasonally weak early summer and start trading strongly at the end of the summer. The summer came and left, the fall came and left, and the year came and left, and still no rally to be seen. No predominant cause for the failure to appear for the market rally, but pointers abound: a) for once, world economic growth prospects have been getting revised lower, from the Japanese economy entering recession and the European economy flirting with one too, b) the Chinese economy downshifting seriously on the back of calls for clean air (i.e. burning less coal) and cleaner business policies (i.e. going hard after corruption and self-dealing) and lowering inventories, c) new or stricter export requirements of commodities by several countries (grains in Argentina, mineral export duties in Jakarta) and neutral shipping trends despite a bumper crop harvest in the US, while d) vessel supply kept increasing (approximately 620 dry bulk vessels were delivered in 2014 y-t-d, 320 were scrapped in the same period for a net increase of more than 3% on a world fleet of about 10,000 dry bulk vessels at the beginning of the year).

Despite the fact that hope springs eternal in shipping, dry bulk asset prices has been shifting lower as well. Financing is still hard to find for most shipowners and with freight rates low, potential buyers want to see compelling opportunities to get enticed to open their wallet. In our business practice, we often see buyers’ typical reaction to proposed sale candidate vessels: “the market is at $X mil as per ‘last done’ for this vessel and we would never buy at market, but we would consider offering at market less 5-10%”, which approach has been chipping lower on prices from previously done price levels. While earlier in the year prices were moving in tandem for modern and older dry bulk vessels (usually, independent and smaller owners buy ‘older’ vessels and shipowners with access to the capital market prefer modern tonnage, as a rule of thumb), as of recent, there is a bifurcation in the market as modern vessels have been holding better their prices while ‘older’ vessels have seen a more pronounced drop in asset pricing. It’s hard to pinpoint the widening of the gap between older and modern tonnage, but access to funding and capital markets (where also fees are much higher, and also where there is the need of ‘deal pressure’ and also the need to ‘feed the beast’) may partially explain the price differential. A partial explanation may also be attributed to the strength of the US Dollar (and / or the weakness of the Japanese Yen) which have made the sale of Japanese-controlled vessels more palatable – and, indeed, we have seen more Japanese controlled tonnage for sale in the secondary market in the last few months.

In the capesize market, we have recently seen the sale by Daichi Chuo of MV ‘First Eagle’ (170,000 dwt, 2010, Imabari Shipbuilding) at approximately $41 million to Chinese buyers. In middle November, Daiichi Chuo again disposed of another larger-sized bulker MV ‘First Ibis’ (180,000 dwt, 201, Universal S.B.) at $45 mil to same buyers, clearly indicating that the price of ‘First Eagle’ is a meaning step-down in pricing, after adjusting for size. As a matter of comparison, Daiichi Chuo again sold another capesize vessel in April this year, MV ‘Shanganfirst Era’ (181,000 dwt, Koyo Dock K.K, 2010) at approximately $54 mil to Greek buyers (Golden Union), which makes clear the asset pricing trend between spring and fall this year. Just recently, publicly listed Diana Shipping announced the acquisition of a 2015-built vessel at $50 mil (Hull No BC18.0-51, 180,000 dwt, Beihai Shipyard, 2015); interestingly, Diana also announced this week in a press release the chartering of one of their 2010-built capesize vessels MV ‘New York’ (177,000 dwt, SWS, 2010) to Clearlake for a period of 14-18 months at $12,850 pd less 5% commissions – it would seem that there is still a big disconnect between asset pricing and freight market, unless there is strong conviction for a market recovery. Back in November, Alpha Tankers and Freighters of Greece acquired from Lauritzen Bulkers the vessel MV ‘Cassiopeia Bulker’ (180,000 dwt, Hanjin H.I., 2011) at approximately $42 mil, while at around the same time financially oriented CarVal Investors acquired MV ‘Mineral Manila’ (180,000 dwt, HHIC-Phil., 2011) at $43 million from Bocimar. As an indication of the present market bifurcation, Turkish interests acquired MV ‘Pacific Triangle’ (185,000 dwt, Samsung, 2000) at close to $17 mil, approximately $5 mil premium over scrap price for a vessel likely to have 5+ years remaining economic life.

The panamax dry bulk market has been experiencing a tough cycle, with very weak rates and many existential questions of the optimal size of a ‘panamax’ vessel in our modern world. In any event, just this week, publicly listed Scorpio Bulkers announced the sale of 81,000 dwt vessel at $30.5 mil to Vita Management in Greece (Hull No 164, Tsuneishi Zhoushan, 2015) – incidentally, this week also Scorpio Bulkers announced the scuttling of a six-vessel capesize order (for the newbuilding orders to be converted for coated aframaxes to be sold to sistership company Scorpio Tankers, another implicit sign of the sorry state of the dry bulk market). Earlier this year, Mitsubishi Corp. sold three post-panamax vessels to Golden Union in Greece at prices reported at approximately $34 mil (Hull No 1623 / MV ‘King Santos’ / MV ‘King Seattle’ 81,000 dwt, STX SB (Jinhae), 2014), making clear the asset price trend since the spring of this year for this asset class (appr. 10% decline). K-Line sold the panamax bulker MV ‘Opal Stream’ (77,000 dwt, Oshima S.B., 2003) at $13.5 mil to BulkSeas, while Daiichi Chuo – still an active seller – sold the vessel MV ‘Mulberry Wilton’ (77,000 dwt, Tsuneishi Zosen, 2004) at $14.5 mil to Greek buyers. As a matter of market trend, back in February 2014, Euroseas acquired the Japanese (Nisshin Shipg. Co.) bulker MV ‘Million Trader II’ at $22.0 mil (77,000 dwt, Tsuneishi Zosen, 2004).

Japanese-built and -owned ultramax bulker ‘Global Success’ in Greek waters (Port of Piraeus) in November 2014… Image source: http://www.basil-karatzas.com

In the handymax / supramax / ultramax markets, the prospects have not been much rosier; there has been a great deal of concern about the outstanding orderbook in the sector, although the economics at present are better pari passu to other asset classes: the freight revenue line is as bad as for bigger vessels but at least the costs basis is of a smaller scale. Crown Shipping sold recently to Ocean Agencies two prompt resales (Hull Nos ZJB-401/-402, 63,000 dwt, Sinopacific, Zhejiang, 2015) at $27 mil, each. In late spring, Da Sin Shipping sold the memorably-named MV ‘Mandarin Wisdom’ (63,500 dwt, Jiangsu Hantong H.I., 2014) at close to $29 mil to Erasmus Investments; at the beginning of 2014, in January, Greek interests acquired MV ‘Dietrich Oldendorff’ (63,500 dwt, Sinopacific Dayang, 2013) at $32 mil; the down-slopping asset trend is obvious since the beginning of the year. Again, Daiichi Chuo has sold MV ‘Sansho’ (55,800 dwt, I.H.I., 2012) at $24.5 mil to European interests; similarly, Japanese-based Noma Kaium sold MV ‘Ruby Halo’ (58,000 dwt, Tsuneishi Cebu, 2011) to First Steamship for $27 mil. For ‘older’ vessels in this sector, K-Line again has recently been active with the sale of MV ‘Mokara Colossus’ (55,800 dwt, Kawasaki S.B., 2006) at $14.5 mil to (again) BulkSeas; British Marine sold MV ‘Gwendolen’ (50,250 dwt, Mitsui Shipbuilding, 2004) at the respectable $14 mil to Gurita Lintas; similarly, LT Ugland Bulk sold MV ‘Emily Manx’ (47,000 dwt, Shin Kurushima, 2001) at $10.25 mil, almost as much as Orient Marine Co. fetched for their MV ‘Pax Phoenix’ (50,250 dwt, Mitsui Shipbuilding, 2001) to Bangladeshi interests. Based on these recent transactions reported, one notices the nature of the sellers (Japanese, predominantly) and the shipbuilding origin of the vessels (Japanese, predominantly again – as there is little tolerance in this market for low quality tonnage); the nomenclature of the sellers re-affirms our earlier comment on FX rates and asset market drivers.

In the handysize market, prominent transactions include the sale of evocatively named MV ‘Brilliant Moira’ (28,500 dwt, I-S Shipyard, 2014) by Aono Kaiun K.K to Greek interests at $18.10 million, and the sale of MV ‘Hudson Bay’ (29,500 dwt, Shikoku Dock, 2011) at $18.4 mil to Dalex Shipping in Greece by Mitsui Warehouse; same sellers have disposed of older vessel MV ‘Durban Bulker’ (32,500 dwt, Kanda S.B., 2005) at $13.5 mil to Taylor Maritime. Phoenix Shipping & Trading has sold the vessel MV ‘Porto Maina’ (18,700 dwt, Yamanishi Zosen, 2008) at $8 mil to European interests. Again, Japanese-originating names dominate sellers and shipbuilders nomenclature.

Volume of transactions overall has been decent and, overall, it’s only marginally lower than 2013 when it was a better market overall. As expected, the beginning of 2014 was more active in terms of transactions, and with the passing of time and asset price declining, volume has been tapering off as well. While overall since 2011 the dry bulk freight market has been improving (Graph 3), the market has been moving within a ‘trading range’, between 1,000 and 2,000 points for the BDI – with the Cape market more ‘expressive’ and reactive, primarily to rhythms from China.

Graph 3: Baltic Dry Indices since January 2011 (data source: The Baltic Exchange)

All eyes are of course on 2015 and many wonder whether the BDI will manage to break out of the ‘trading range’. But again, many wonder whether any of the presents the Three Maghi (Three Wise Men) brought were a ‘market catalyst’ for a better market… gold, frankincense and myrrh don’t seem to be good enough…

Merry Christmas!

© 2013-2014 Basil M Karatzas & Karatzas Marine Advisors & Co. All Rights Reserved.

IMPORTANT DISCLAIMER: Access to this blog signifies the reader’s irrevocable acceptance of this disclaimer. No part of this blog can be reproduced by any means and under any circumstances, whatsoever, in whole or in part, without proper attribution or the consent of the copyright and trademark holders of this website.Whilst every effort has been made to ensure that information herewithin has been received from sources believed to be reliable and such information is believed to be accurate at the time of publishing, no warranties or assurances whatsoever are made in reference to accuracy or completeness of said information, and no liability whatsoever will be accepted for taking or failing to take any action upon any information contained in any part of this website. Thank you for the consideration.