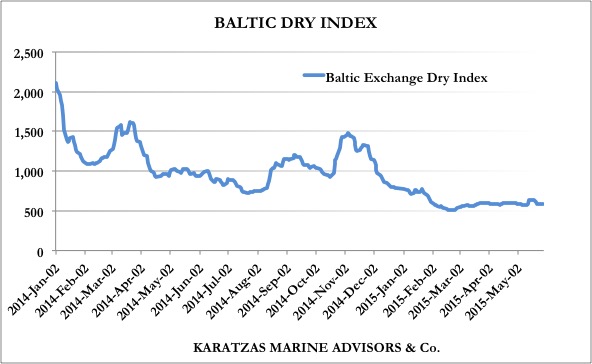

The Baltic Dry Index (BDI) established a 30yr low point in February this year; actually the lowest reading of the index ever. Since then, the market has been bouncing along the bottom with a very anemic improvement to show since then. There are concerns that the industry has entered a long-term phase of malaise with chronic oversupply of tonnage; certain trends point to such direction such as massive orders by cargo interests and end users building up their own fleets (i.e. Cosco, Vale, etc) that will make life for independent dry bulk owners difficult, or at the very least ‘shave the market peaks’. China is done for now with their exponential growth of their market as they try to position their economy towards services and focus on a more equal distribution of wealth that can assure social peace. There also have been structural shifts in the markets associated with shipping, such as replacement of coal with natural gas for electricity and power generation; at present the trend against coal is so bad that it seems coal is becoming a ‘four letter word’ as investors, institutions and sovereign funds are competing for the fastest exit from the industry; for sure, natural gas will need also shipping but not on dry bulk vessels; and the coal trade as almost as big as iron ore at almost 1.2 bln tonnes of coal expected to be transported this year vs. 1.5 bln tonnes of iron ore, based on data by Karatzas Marine Advisors & Co.

Baltic Dry Index: not a day at the beach, regrettably! (Karatzas Marine Advisors & Co.)

Most institutional investors and shipping banks have turned their backs on the dry bulk market, at least for now; thus, there is extremely limited liquidity, which further compounds the downward pressure on dry bulk asset pricing that are inflicted by the weak freight market. The main sources of financing for dry bulk projects today are from the capital markets (selectively available and often at a substantial discount; $SALT’s secondary offering at 30% discount is a clear example of a fallen angel) or with sweat equity and own equity. Independent shipowners and sweat equity have their own capital limitations and likely to opt for older tonnage at rock-bottom pricing, mostly looking for vessels older than 15yrs of age at about scrap pricing; if one has access to cargo or charterers or niche markets, buying a vintage bulker at scrap is not a bad investment proposition: for a few million dollars (small amounts in absolute terms that can be afforded by individual investors) and with minimal capital at risk (premium over scrap), if a buyer can squeeze a few year’s of economic life out of cigarette-butt (think of Benn Graham and Warren Buffett), what can go wrong? And, if the market unexpectedly recovers, these buyers will have hit the jackpot. The access to capital accurately reflects the market dynamics and asset pricing, as big, cash-rich, prime buyers go for beaten-down prices of modern, top quality tonnage, while small, cash-rich owners with access to cargo go for bottom-fishing; thus, there is relative demand from buyers on the opposing ends of the spectrum while demand is sagging for middle-aged vessels; for those involved with volatility analysis and option trading, what’s happening in the dry bulk market reminds of a so-called ‘volatility smile’.

Activity in the dry bulk market is ebbing and flowing, but mostly ebbing as most buyers are taking their sweet time before make any decisions, to buy at all, and if so, at what price. Since asset prices are low and most of the market really is focused on older and cheap tonnage, sale & purchase commissions often are laughable, putting pressure on many smaller brokerage houses.

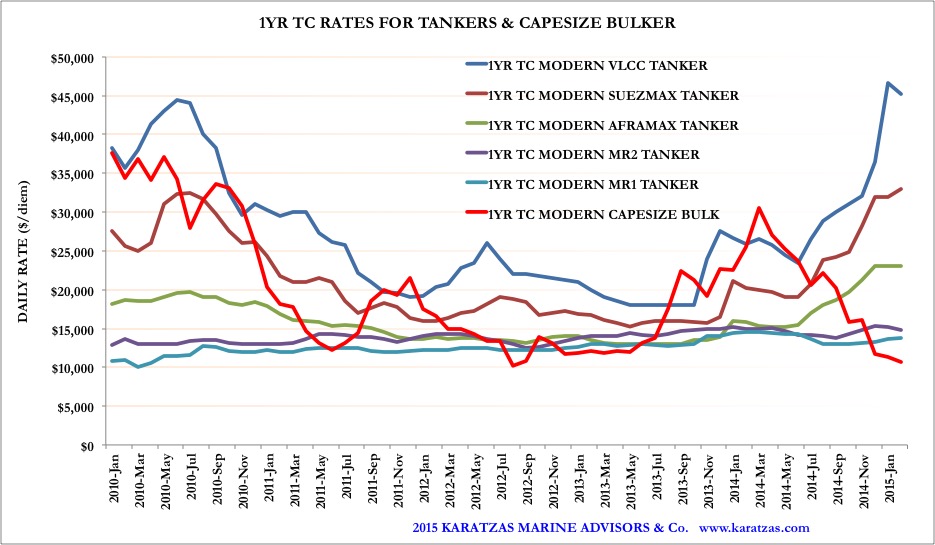

In the capesize market, Scorpio Bulkers (ticker: SALT) has been continuing their selective divestment of assets in an effort to fill the funding gap for their massive newbuilding program (along with their discounted pricing of secondary offerings as announced earlier this week for 133,000,000 shares of common stock at $1.50 per share; the stock was trading well above $2.20/share at the time of the announcement). In early April, Scorpio has sold three units of capesize bulkers at $44 mil each (2015/2016 deliveries of 180,000 dwt tonnage at Daewoo-Mangalia, MV ‘SBI Churchill’, MV ‘SBI Perfecto’ and MV ‘SBI Presidente’) while this week it has been reported that additional sales took place at $41 mil each, indicating an 8% drop in asset pricing in approximately two months (MV ‘SBI Corona’, MV ‘SBI Estupendo’ and MV ‘SBI Diadema’, 180,000 dwt, 2016, Shanghai Waigaoqiao/China). Approximately one month ago, the still modern cape MV ‘Blue Everest’ (180,000 dwt, 2010, Daehan) was sold at $27 mil, and the older MV ‘Jiang Jun Shan’ (177,000 dwt, 2006, Namura) was sold at $18.2 million. Most market reports have a standardized 5yr-old cape at $30 mil ($29.2 mil as per the Baltic Exchange Sale & Purchase Assessment Index (BSPA)), while just one year ago, such number was pushing the $50 mil mark ($49.08 mil as per BSPA); this is a monumental illustration is value destruction, where $20 mil per vessel has evaporated into thin air, a 40% drop. Few people could have envisioned such a market decline (at least not us, we have to confess), but for professional asset managers, institutional investors, portfolio managers, private equity funds and shipowners on roadshows pounding the table about the market getting this so wrong is a humbling example to watch and wonder.

In the panamax market, MV ‘Navios Esperanza’ (75,000 dwt, Universal S.B., 2007) was sold to $14 mil with her intermediate survey due. Interestingly, MV ‘F.D. Jacques Fraubart’ (76,500 dwt, Imabari S.B. Marugame, 2007) was sold less than six months ago at $19 mil, indicating the magnitude of the asset declines in this sector; presuming appr. $1 mil for the cost of the intermediate survey, this sale represents more than 25% decline in less than six months. The sale of the MV ‘Navios Esperanza’ however is in line with present market given than two weeks ago MV ‘Lowlands Queen’ (76,500 dwt, Imabari S.B. Marugame, 2008) was sold at $15 mil. Decade-old tonnage in this segment has just been decimated as recently the Japanese-built MV ‘Million Trader’ (76,500 dwt, Tsuneishi Zosen, 2004) was sold for appr. $9.5 mil; given that the salvage value of the vessel is $4.5 mil in the present market, she’s Japanese-built and her remaining economic life is more than ten years (fifteen actually remaining years as far design life is concerned), it is hard to see how this can be a bad investment, negative cash flows in the immediate future notwithstanding. And, the market is so terrible for pricing panamax bulkers of this vintage that actually the sale of MV ‘Million Trader I’ (76,000 dwt, Tsuneishi Zosen, 2006) at $12 mil in early May was actually considered at ‘overpriced’ territory by one prospect buyer. Similar and tonnage and pricing, MV ‘Medi Sinagpore’ (75,500 dwt, Universal S.B., 2006) was sold for $12.8 mil while the slightly older MV ‘Rose Atlantic’ (75,500 dwt, Sanoyas, 2005) at $11.0 mil. As a matter of comparison, this time last year, the consensus estimate for a 5yr old panamax bulkers was standing at $26 mil ($26.9 mil as per BSPA index), while now the market stands at appr. $17 mil ($16.4 mil as per BSPA), representing an impressive 40% drop in asset prices.

In the ultramax / supramax market, Norden A/S has disposed of two 60,000 dwt Ultramax newbuildings at Oshima Shipbuilding for delivery in Q4-2015 and Q1-2016 for a price in the region of $25m each (N/B RESALE HULL 10781 / 10782, Oshima Shipbuilding, 2015/2016); EastMed of Greece has been reported as buyers. Similarly sized tonnage but older, MV ‘Nord Liberty’ (58,750 dwt, Tsuneishi Cebu, 2008, 4x30T cranes) was sold to Sea World Management for a price region $12.5 mil. The lightly newer MV ‘Hudson Trader II’ less than a month ago (58,00 dwt, Tsuneishi Zhoushan, 2009) had achieved a more respectable $14.2 mil. From Nisshin Shpg.Co.Ltd. Again, as a matter of comparison, BSPA for a modern surpramax was standing at $25.8 mil this time last year and only at $15.46 mil at present; as painful as it has been, supramaxes / ultramaxes / handymaxes have been another great way of value destruction since last year.

Wishing that all waters in shipping were so clear to read! (Image source: Karatzas Photographie Maritime)

While dry bulk asset prices have dropped substantially over the last year, the consensus is that is the ‘glass is half empty’, still. There many reasons to think so, given still the outstanding orderbook to be delivered, excess shipbuilding capacity, low interest rates and excess liquidity for certain markets, mentions of additional credit lines for export credit from China, and lots and lots of dry powder from institutional investors that can move the market at any given point. On the other hand, as we outlined in a recent post, smart money are getting a second look on certain types of vessels in the dry bulk market. Prices are low enough to be tempting, despite negative cash flows in the near term that will have to be ‘added’ to any purchase price; however, delays in deliveries are negotiated each day from buyers, newbuilding orders have stopped – to the delight and surprise of many a shipowner, charterers have gone on a limp to stay away from the period market and delay as much as possible their chartering requirements. There are some smart money that have start thinking that most of the bad news have been priced in the market and, at least in the near future, any surprises likely to have a positive effect on the market. Maybe it’s time to start seeing the dry bulk glass as half-full.

© 2013-2015 Basil M Karatzas & Karatzas Marine Advisors & Co. All Rights Reserved.

IMPORTANT DISCLAIMER: Access to this blog signifies the reader’s irrevocable acceptance of this disclaimer. No part of this blog can be reproduced by any means and under any circumstances, whatsoever, in whole or in part, without proper attribution or the consent of the copyright and trademark holders of this website.Whilst every effort has been made to ensure that information herewithin has been received from sources believed to be reliable and such information is believed to be accurate at the time of publishing, no warranties or assurances whatsoever are made in reference to accuracy or completeness of said information, and no liability whatsoever will be accepted for taking or failing to take any action upon any information contained in any part of this website. Thank you for the consideration.